In accordance with Articles 10 and 11 of the Master Plan of the Development of the Guangdong-Macao In-Depth Cooperation Zone in Hengqin (the “Plan”) promulgated by the State Council on 5 September 2021, eligible enterprises in the Guangdong-Macao In-Depth Cooperation Zone in Hengqin (the “Cooperation Zone”) are subject to a reduced corporate income tax (CIT) rate of 15%. As for the tourism, modern services and high technology businesses set up in the Cooperation Zone, the newly added earnings from overseas direct investment will be exempted from CIT. Domestic and international high-end talents and talents in short supply working in the Cooperation Zone shall be exempted from individual income tax (IIT) on the taxable income exceeding 15%.

To implement the above policy, the Department of Finance of Guangdong Province firstly forwarded the preferential IIT policies of the Ministry of Finance and the State Taxation Administration in the Cooperation Zone (“Circular No. 3”) in March 2022 to further clarify the relevant contents of the preferential policies. The Economic Development Bureau of the Cooperation Zone issued the Notice on Pre-registration of High-end Talents in Short Supply Entitled to Preferential Policies on Individual Income Tax in the Guangdong-Macao In-Depth Cooperation Zone in Hengqin (“Pre-registration Notice”), and officially started the 2021 pre-registration in February 2022.

On 1 June 2022, the Ministry of Finance and the State Taxation Administration officially issued Cai Shui [2022] No. 19 Announcement (“Announcement No. 19”), which clarified several preferential CIT policies in the Cooperation Zone set out in the Plan and provided the latest version of the Catalogue of Corporate Income Tax Concessions (2021 Version) (the “Concession Catalogue”). So far, most of the preferential CIT and IIT policies in the Cooperation Zone set out in the Plan have been implemented and refined. In this article, we will provide an overview of the implementation of the preferential policies in the Cooperation Zone.

CIT

In accordance with the Announcement No. 19, there are three preferential CIT policies in the Cooperation Zone: a reduced CIT rate of 15%; tax exemption for income from overseas direct investment; and one-off deduction for capital expenditure.

I. 15% CIT rate

Eligible enterprises will enjoy a reduced CIT rate of 15% under the Announcement No. 19. The specific requirements are as follows:

1. An enterprise is allowed to enjoy the preferential policies only when its main business falls within the scope specified in the Concession Catalogue (see Appendix I), and the revenue from its main business accounts for more than 60% of its total revenue;

2. The actual management body of the enterprise intending to enjoy the preferential policies is required to be located in the Cooperation Zone, and it shall exercise substantial management and control over the production and operation, personnel, accounts and property of the enterprise; and

3. For enterprises whose head office is located in the Cooperation Zone, the 15% tax rate applies only to the income of their eligible head office and branches located in the Cooperation Zone; for enterprises whose head office is located outside the Cooperation Zone, the 15% tax rate applies only to the income of their eligible branches located in the Cooperation Zone.

II. Tax exemption for income from overseas direct investment

Under the Announcement No. 19, the tourism, modern service and high-tech enterprises established in the Cooperation Zone shall be exempted from CIT for income derived from new overseas direct investment if:

1. Such income is the business profits derived from newly established overseas branches, or dividends corresponding to new overseas direct investment which is obtained from overseas subsidiaries in which the enterprise holds 20% (inclusive) equity;

2. The statutory CIT rate in the invested country (region) is not less than 5%.

3. The Concession Catalogue (see Appendix I) shall be followed for requirements on tourism, modern service and high-tech industries.

III. One-off deduction for capital expenditure

In accordance with the Announcement No. 19, a one-off pre-tax deduction or accelerated depreciation and amortisation is allowed for eligible capital expenditures of an enterprise in the period in which such expenditures are incurred. The specific requirements are as follows:

1. For any newly acquired asset with a unit value of less than RMB 5 million (inclusive), the expenditure for such asset is allowed to be included in the costs and expenses of the current period on a one-off basis and deducted when calculating the taxable income, and depreciation and amortisation will no longer be calculated on a yearly basis;

2. For any newly acquired asset with a unit value of more than RMB 5 million, the depreciation and amortisation period may be shortened or accelerated depreciation and amortisation applied.

IIT

I. Applicable target

Pursuant to the Circular No. 3 and the Pre-registration Notice, the domestic and overseas high-end talents and talents in short supply working in the Cooperation Zone shall be exempted from IIT on the taxable income exceeding 15%.

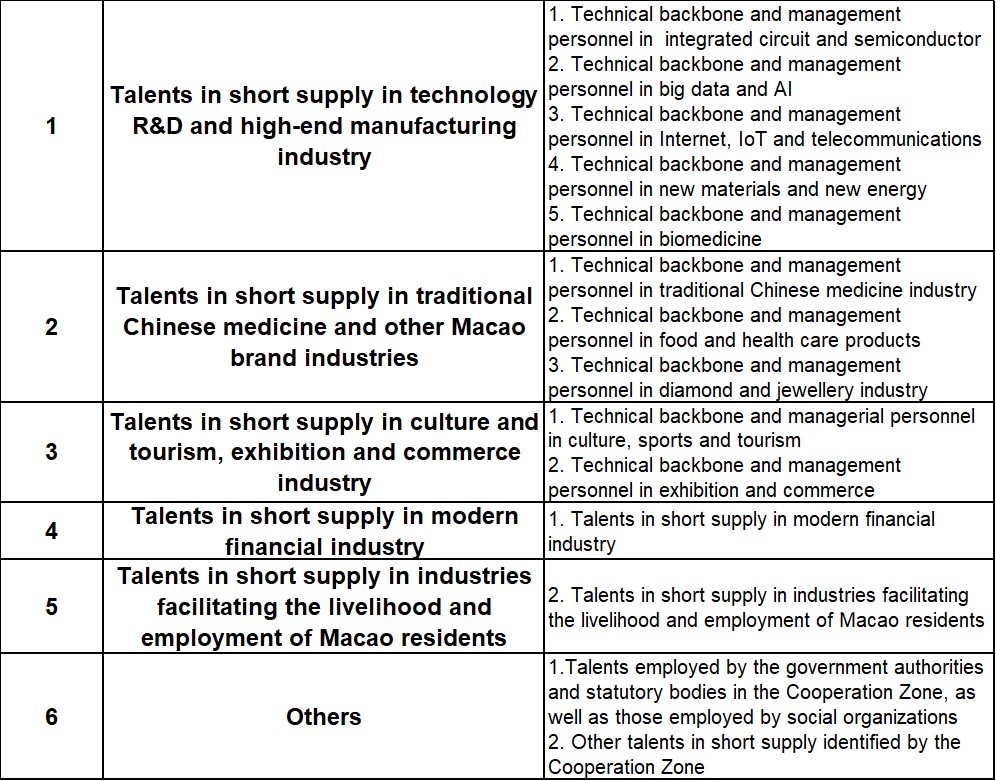

The talents refer to those who work in technology, R&D and high-end manufacturing industry, traditional Chinese medicine and other Macao brand industries, culture and tourism, exhibition and commerce industry, modern financial industry and other new industries that promote the diversified development of Macao’s economy, and who satisfy the requirements set out in the Catalogue of Pre-registration of Talents in Short Supply in Demand in the Guangdong-Macao In-Depth Cooperation Zone in Hengqin (“Catalogue of Demand”) (see Appendix II).

II. Application requirements:

1. High-end talents included in the list for management are high-caliber talents identified by the Executive Committee of the Cooperation Zone.

2. The talents in short supply included in the list for management refer to those who satisfy the requirements set out in the Catalogue of Demand (see Appendix II) and meet one of the following conditions:

(1) Having a bachelor's degree or above, or an overseas equivalent qualification (degree) recognised by the Ministry of Education;

(2) Having professional and technical qualifications at the assistant level or above; or

(3) Being a qualified technician or higher skilled personnel who has obtained the national vocational qualification certificate.

3. The high-end talents and talents in short supply should also meet the following requirements:

(1) Working in the Cooperation Zone and paying taxes in accordance with the law; complying with the laws and regulations and supporting the policy of “one country, two systems”; and paying social insurance in the Cooperation Zone for more than 6 consecutive months in a tax year (including December of that tax year);

(2) Providing evidentiary materials on labour relationship, such as labour contracts or employment agreements with a term of more than one year signed with entities registered and operating substantively in the Cooperation Zone.

(a) The labour contract with a term of more than one year (within the valid term ) of an applicant within the statutory working age shall be subject to the employment registration filing. Social insurance refers to that paid in the name of the employer in the Cooperation Zone in accordance with the law. The employment registration filing and payment of social insurance premiums shall be subject to the verification results of the information from the Zhuhai Municipal Government Services Data Management Bureau.

(b) Overseas talents and domestic talents above the statutory retirement age who are exempted from participating in social insurance programs pursuant to the relevant provisions shall upload evidentiary materials, such as written labour contracts or employment agreements with a term of over one year concluded with entities registered and operating substantively in the Cooperation Zone (The contracts or agreements shall be in the valid period).

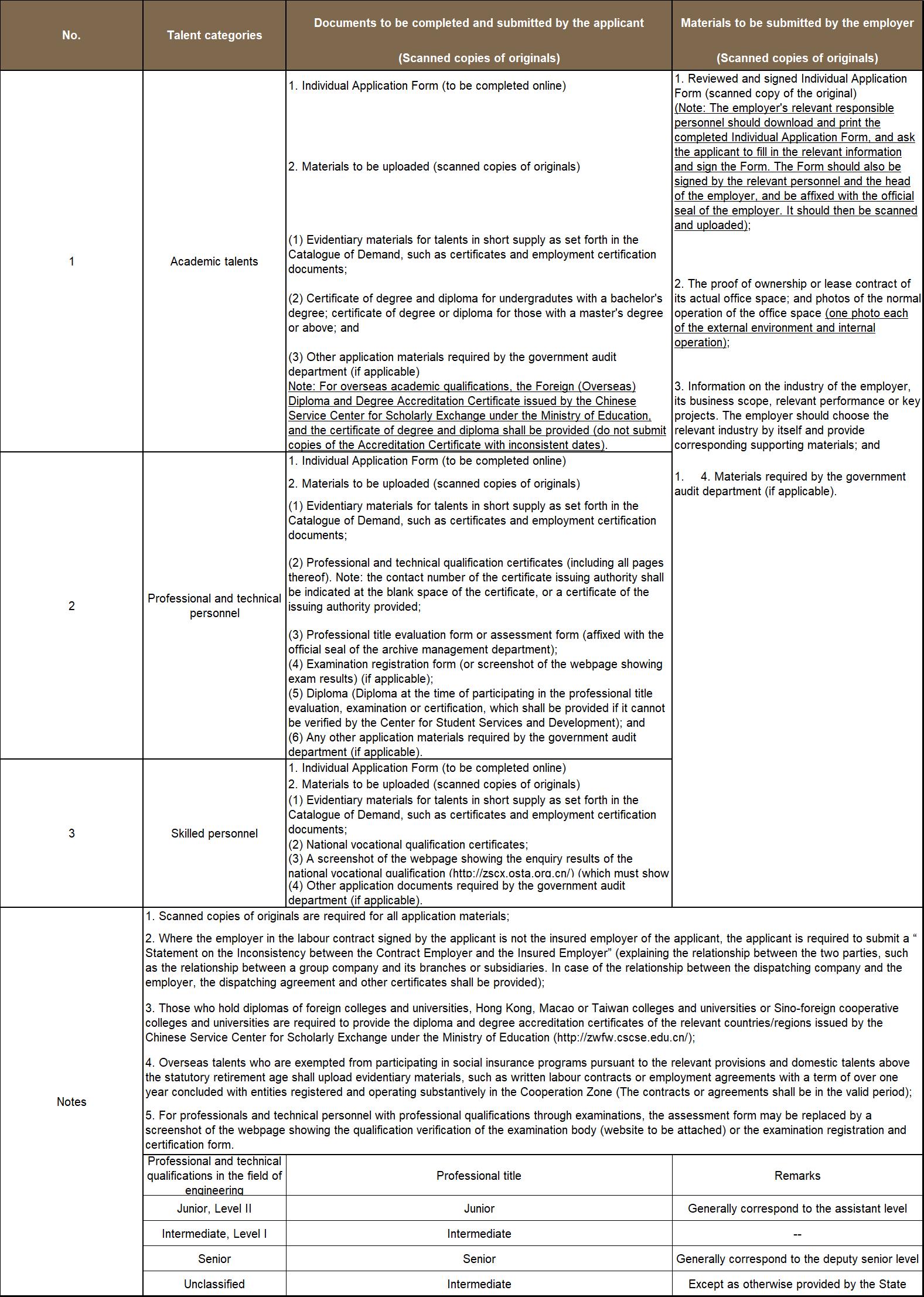

III. Materials required:

IV. Flow chart for application

Policy application

In applying the above tax incentives in practice, the following four issues deserve our continuous attention:

I Talent classification catalogue to be further refined

At the beginning of this year, the Executive Committee of the Cooperation Zone issued a catalogue of talents in short supply (see Appendix II) when conducting the pre-registration of high-end talents and talents in short supply. The catalogue, however, is only applicable at the pre-registration stage, and the catalogue of talents who are entitled to exemption of IIT on the taxable income exceeding 15% remains to be released. As the scope of the catalogue for CIT incentives greatly expands, the scope of the catalogue for IIT incentives will also be further expanded. We hope that the latter will be released as soon as possible to further attract domestic and overseas talents to work in the Cooperation Zone.

II Main business and substantial operations

Enterprises seeking the above tax incentives should first determine whether their main business falls within the scope of the industries listed in Appendix I. In practice, however, the businesses of many enterprises are so complicated that it is difficult to define what is their main business. In accordance with Article 5 of the Announcement No. 19, tax authorities may request the relevant administrative department of the People’s Government of Guangdong Province or its subordinate administrative department authorised thereby to issue relevant opinions if it has difficulties in determining whether an enterprise’s main business falls within the scope set out in the Concession Catalogue.

In addition, the Announcement No. 19 clearly provides another prerequisite for enjoying the CIT incentives, i.e., an enterprise shall conduct substantial operations in the Cooperation Zone. In other words, the actual management body of the enterprise shall be located in the Cooperation Zone, and it shall exercise substantial management and control over the production and operation, personnel, accounts and property of the enterprise. The Announcement No. 19, however, does not expressly provide specific requirements for “substantial operations”, which remains to be further clarified based on practical experience or detailed rules.

III Valid period

It is noteworthy that, unlike similar policies in other regions in China which usually have a valid period, no fixed valid period is set for the preferential CIT policies in the Cooperation Zone. This reflects the State’s determination to develop the economy of the Cooperation Zone and promote the integrated development of Guangdong and Macao in the long run.

The preferential IIT policies in the Cooperation Zone will expire on 31 December 2025, and it remains to be seen how these policies will be continued and adjusted after the expiration.

IV Tax reduction

The above-mentioned preferential tax policies of “taxable income of individuals exceeding 15% shall be exempted from tax” and “eligible enterprises may enjoy a reduced CIT rate of 15%” are, according to the general accounting principles, “direct tax deduction”, which are different from the “rebate after collection” approach. We will continue to pay attention to the practice of the relevant authorities on direct tax deductions.

To sum up, the preferential policies on CIT and IIT in the Cooperation Zone have been greatly refined on the basis of the Plan, which provides a basis for the application of relevant tax incentives to enterprises and individuals. It is expected that the application of the preferential policies will be more specific and clearer based on practical experience and further clarified supporting documents. In addition, the planned customs closure operation of the Cooperation Zone at the end of this year, coupled with the further refinement of the preferential tax policies will certainly attract domestic and overseas talents and enterprises to the Cooperation Zone, promoting the further development of the Cooperation Zone and the diversification of Macao's industries.

Appendix

The Catalogue of Pre-registration of Talents in Short Supply in Demand in the Guangdong-Macao In-Depth Cooperation Zone in Hengqin